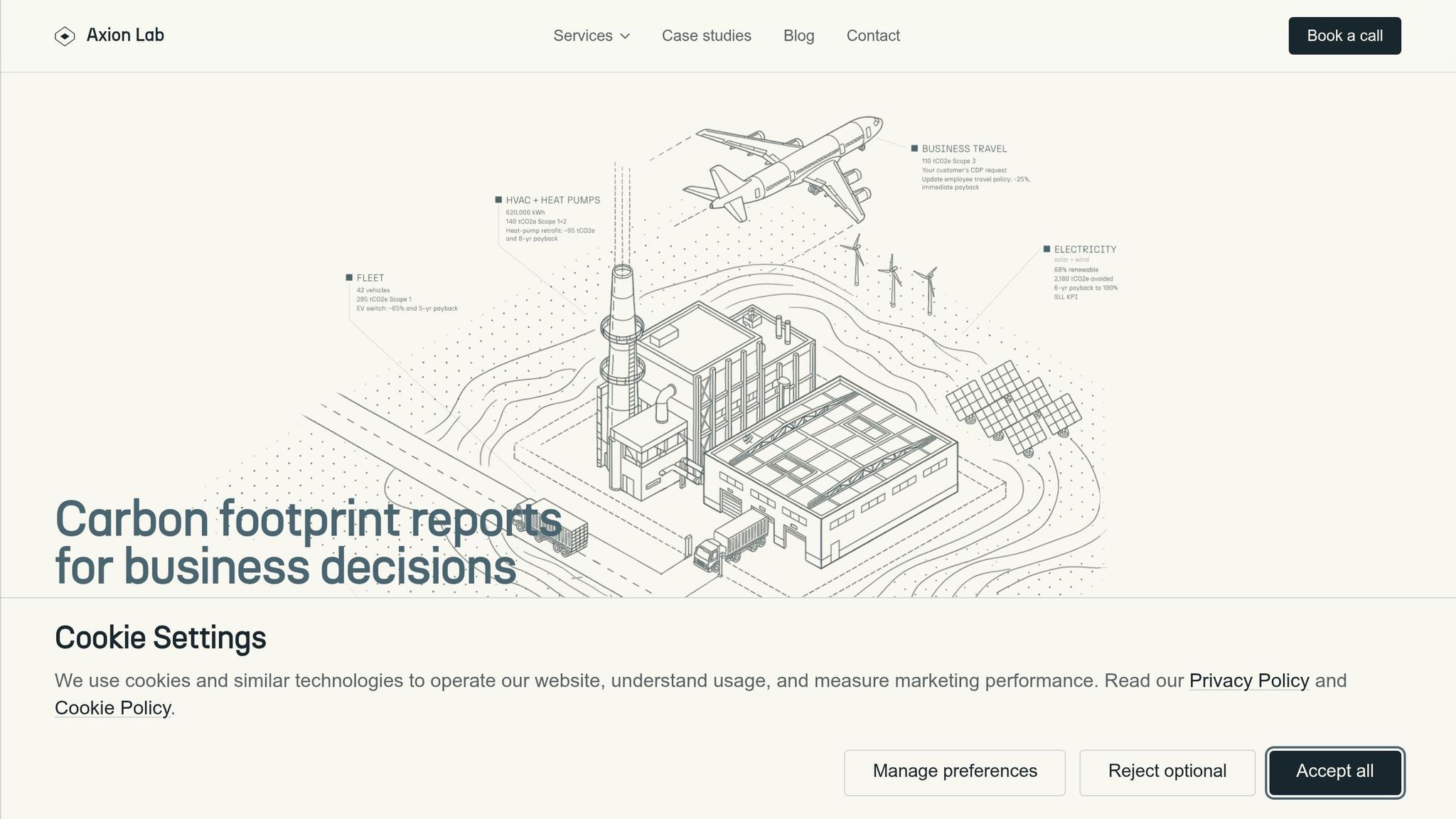

The GHG Protocol is the global standard for measuring and managing greenhouse gas (GHG) emissions. It categorises emissions into three scopes:

- Scope 1: Direct emissions from owned or controlled sources (e.g., company vehicles, on-site fuel use).

- Scope 2: Indirect emissions from purchased energy (e.g., electricity, heating, cooling).

- Scope 3: Indirect emissions across the value chain (e.g., suppliers, product use). These often account for over 70% of a company’s total emissions.

Why does it matter? Nearly all major reporting frameworks - like CDP, SBTi, and the EU’s CSRD - are based on the GHG Protocol. It ensures emissions data is consistent, comparable, and reliable, making it indispensable for businesses and investors.

Key facts:

- Used by 97% of S&P 500 companies reporting to CDP (2023).

- Covers seven GHGs, including CO₂, CH₄, and N₂O.

- Managed by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD).

For private equity and ESG analysts, understanding the GHG Protocol is crucial for evaluating climate risks, ensuring accurate emissions reporting, and meeting regulatory requirements.

GHG Protocol Standards Suite: Scopes, Frameworks & Key Stats

Who Maintains the GHG Protocol?

The roles of WRI and WBCSD

The GHG Protocol is managed through a partnership between the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD). This collaboration, which began in 1998, was designed to create a unified framework for measuring emissions [2].

WRI brings expertise in data analysis and global policy, while WBCSD, a coalition of CEOs from major companies generating over USD $8.5 trillion in revenue and employing 19 million people, ensures the standards are practical for businesses [2].

"The popularity of GHG Protocol standards and guidance is due in part to the widespread stakeholder outreach and consultation that is facilitated by WRI and WBCSD during each standard development project." - GHG Protocol [1]

The development of these standards involves a formal, multi-stakeholder process that includes input from governments, businesses, NGOs, and industry experts. The governance structure behind this process features a Steering Committee, an Independent Standards Board, and Technical Working Groups to ensure both technical rigour and broad consensus [2].

How often the standards are updated

The GHG Protocol's standards are updated as needed to reflect new scientific findings, regulatory changes, and practical insights. These updates follow a thorough process that incorporates feedback from a wide range of stakeholders. For instance, the Corporate Standard's 2004 revision was the result of a two-year dialogue involving over 350 experts from various sectors, including businesses, NGOs, and governments [8]. Similarly, the 2015 Scope 2 Guidance introduced a major methodological shift, requiring companies to report emissions using both location-based and market-based methods to account for the increasing use of renewable energy certificates.

In 2023, a new round of updates began for the Corporate Standard, Scope 2 Guidance, and Scope 3 Standard. This initiative aims to ensure the framework remains aligned with modern requirements, such as the EU's Corporate Sustainability Reporting Directive (CSRD) [5]. By April 2026, new Joint Working Groups had been formed to continue this revision process [2].

Why governance matters in private markets

The rigorous and transparent update process of the GHG Protocol is essential for its credibility, particularly in private markets. Investors and due diligence teams rely on strong governance to ensure emissions data are consistent and independently reviewed. This transparency provides a reliable foundation for evaluating portfolio companies' emissions data.

The protocol's credibility stems from its multi-stakeholder approach, which positions it as a neutral benchmark. Its five guiding principles - Relevance, Completeness, Consistency, Transparency, and Accuracy - serve as a checklist for evaluating the quality of emissions disclosures [7]. Alignment with regulatory frameworks like CSRD and the expectations of investors further reinforces trust in the protocol. This makes the GHG Protocol the cornerstone for nearly all emissions reporting frameworks developed since.

sbb-itb-6ca8558

The GHG Protocol Standards Suite Explained

The GHG Protocol offers a set of standards tailored to different levels of emissions accounting. Knowing which standard to use is crucial for organisations involved in emissions reporting or conducting due diligence. Together, these standards serve as the accounting framework that supports regulatory policies and due diligence practices mentioned throughout this discussion.

Corporate Accounting and Reporting Standard

This standard forms the backbone of the GHG Protocol. Developed with input from a broad range of stakeholders, the Corporate Standard outlines how organisations can create a comprehensive greenhouse gas inventory across their operations [3]. It addresses seven key gases - CO₂, CH₄, N₂O, HFCs, PFCs, SF₆, and NF₃ - and introduces the well-known Scope 1 and Scope 2 framework.

- Scope 1: Covers direct emissions from sources owned or controlled by the organisation.

- Scope 2: Encompasses indirect emissions from purchased electricity, heat, steam, or cooling.

The standard also provides guidance on defining organisational and operational boundaries.

"The GHG Protocol Corporate Standard has been designed to be program or policy neutral. However, it is compatible with most existing GHG programs and their own accounting and reporting requirements." - GHG Protocol [3]

Corporate Value Chain (Scope 3) Standard

While the Corporate Standard addresses emissions within direct operations, it doesn’t account for emissions across the broader value chain. For many businesses, these emissions - spanning supply chains, logistics, product use, and disposal - represent a significant portion of their total footprint. The Scope 3 Standard, introduced in 2011 after extensive consultation with 2,300 participants from 55 countries, fills this gap [4].

It breaks down value chain emissions into 15 categories, split between:

- Upstream activities: Includes purchased goods and services, business travel, and capital goods.

- Downstream activities: Covers areas like the use of sold products and end-of-life treatment.

For private equity firms, Category 15: Investments is particularly noteworthy, as it provides a framework for calculating emissions at the portfolio level. Companies like Kraft Foods played a key role in shaping this standard through early testing and inventory work in 2010 [4].

"For many businesses, value chain (scope 3) emissions account for more than 70 percent of their carbon footprint. Measuring and managing these emissions can motivate a company to do business with greener suppliers, improve the energy efficiency of its products, and rethink its distribution network." - GHG Protocol [4]

While the Corporate and Scope 3 standards focus on emissions at organisational and value chain levels, other protocols address specific projects and products.

Project and Product Standards

The GHG Protocol also provides tools for more targeted emissions assessments.

- Project Protocol: This standard, developed over four years with input from over 100 experts and 20 project developers across 10 countries, focuses on quantifying emissions reductions from specific mitigation projects. Examples include renewable energy installations, efficiency upgrades, or carbon removal initiatives. This methodology is essential for investors assessing the impact of decarbonisation projects or verifying carbon credits [9].

- Product Life Cycle Standard: This standard evaluates emissions at the product level, covering every stage from raw material extraction to manufacturing, use, and disposal. It helps organisations pinpoint emissions hotspots and improve efficiency. Road-tested by 38 companies in 2010, it remains a key tool for identifying design risks and opportunities in product lines [6]. By February 2026, the GHG Protocol aims to release a harmonised product-level standard in collaboration with ISO to ensure global alignment [6].

Both standards align with international guidelines like ISO 14064, reinforcing their role in emissions reporting frameworks. They allow investors to go beyond company-wide assessments and focus on the climate impact of specific assets, products, or initiatives.

| Standard | Level of Analysis | Investor Application |

|---|---|---|

| Corporate Standard | Organisation-wide | Assessing total carbon liability of a company [3] |

| Scope 3 Standard | Value chain (15 categories) | Identifying supply chain risks and portfolio emissions [4] |

| Product Standard | Individual product/service | Spotting efficiency gains and design risks in product lines [6] |

| Project Protocol | Specific mitigation activity | Quantifying the impact of decarbonisation projects [9] |

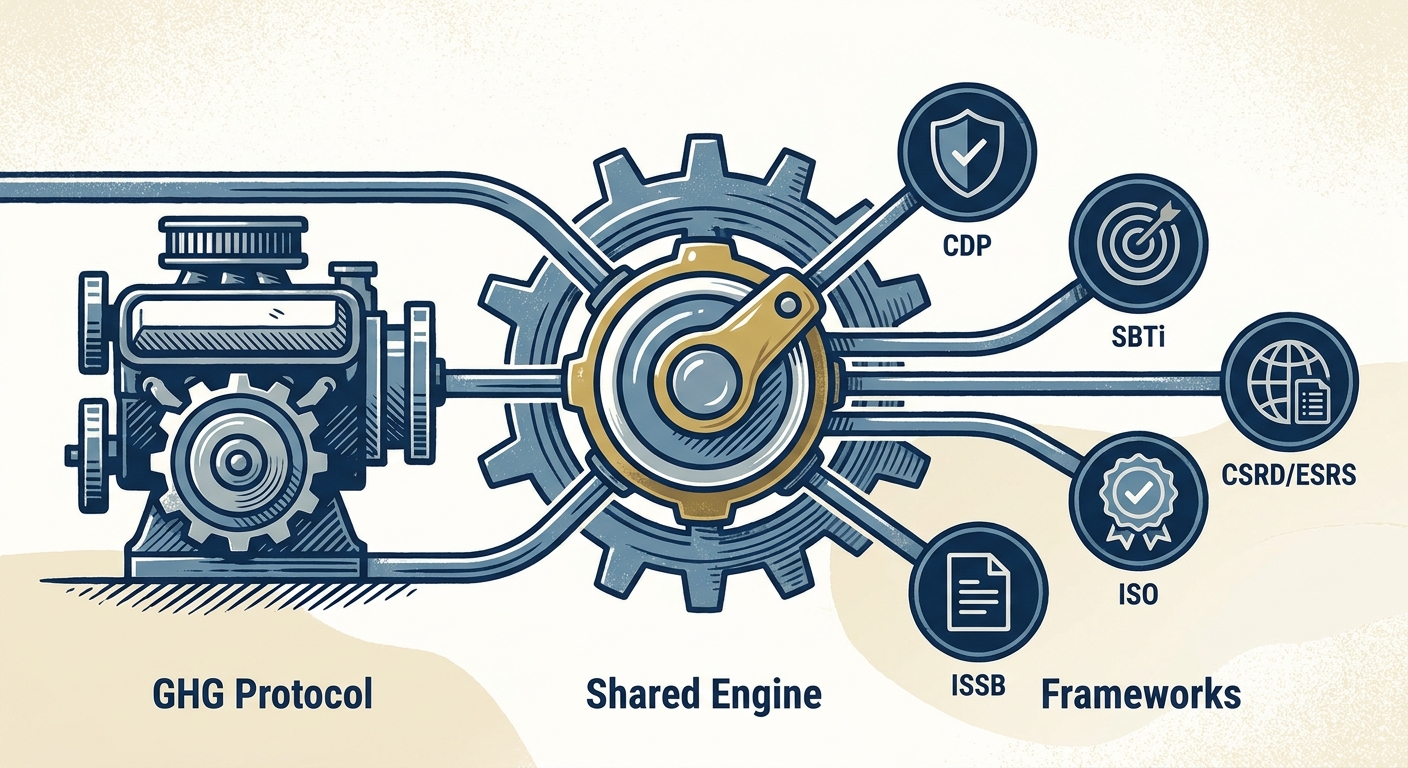

How Other Frameworks Build on the GHG Protocol

The GHG Protocol serves as the cornerstone for nearly all emissions reporting frameworks in use today. Think of it as the shared engine that powers various reporting requirements. This interconnectedness means that a single, well-organised emissions inventory can meet the needs of multiple frameworks simultaneously. Let’s explore how specific frameworks build on and rely on GHG Protocol data.

How the GHG Protocol Relates to ISO 14064

Both the GHG Protocol and ISO 14064 share a scientific foundation, relying on similar emission factors like IPCC Global Warming Potentials and covering the same seven greenhouse gases. However, their purposes differ. The GHG Protocol is designed for voluntary disclosure, offering a detailed methodology, while ISO 14064-1 is an auditable international standard that mandates third-party verification [10]. ISO 14064-1 also categorises emissions into six distinct groups, providing more detail for indirect emissions compared to the GHG Protocol’s three-scope model.

"ISO 14064-1 was written to accommodate a wide range of organisational structures... where the GHG Protocol's three approaches may not fit neatly." - Dr. Nikhitha KK, Senior Manager, Sustainability Assurance [10]

By using the GHG Protocol as a foundation and adapting documentation to meet ISO 14064-1 standards, organisations can streamline the third-party verification process [10].

How CDP and SBTi Use the GHG Protocol

The GHG Protocol also underpins major climate initiatives like CDP and SBTi, both of which depend on its data framework. CDP questionnaires align with the GHG Protocol’s Scope 1, 2, and 3 classifications, allowing companies to directly use their GHG Protocol inventories for disclosure. By 2016, 92% of Fortune 500 companies responding to CDP were already using the GHG Protocol [7].

SBTi goes a step further by leveraging GHG Protocol data to evaluate whether a company’s emissions reduction targets align with the Paris Agreement’s 1.5°C goal [7]. While the GHG Protocol focuses on how to measure emissions, SBTi determines how much needs to be reduced. For SBTi compliance, companies must screen all 15 Scope 3 categories when setting targets, making a comprehensive Scope 3 inventory essential for meaningful climate action [7].

"The GHG Protocol provides the measurement methodology for calculating emissions - it tells you how to measure your carbon footprint. The Science Based Targets initiative (SBTi) uses GHG Protocol data to set reduction targets aligned with climate science." - Konstantinos Kouzelis, Founder & CEO at Coolset [7]

GHG Protocol Alignment Under CSRD and ESRS

The GHG Protocol’s influence has extended into regulatory frameworks like the EU’s Corporate Sustainability Reporting Directive (CSRD) and the European Sustainability Reporting Standards (ESRS). Under CSRD, the GHG Protocol has shifted from being a voluntary guideline to a legal requirement for companies that fall within its scope. Specifically, ESRS E1 (Climate Change) mandates that organisations disclose Scope 1, 2, and 3 emissions using GHG Protocol methodologies [7]. The GHG Protocol outlines how to calculate emissions, while ESRS E1 specifies what to disclose, including transition plans and financial impacts [11].

Although the Omnibus I Directive (set for February 2026) reduced the number of companies under CSRD from approximately 50,000 to 5,000 [11], climate reporting remains a priority. EFRAG’s 2025 analysis revealed that 98% of in-scope companies identified ESRS E1 as a material topic [11].

However, there are technical nuances to address. ESRS E1 requires dual reporting of Scope 2 emissions (using both location- and market-based methods), screening of all 15 Scope 3 categories with documented exclusions for immaterial ones, and updated GWP values based on IPCC AR6 (the GHG Protocol still references AR5) [11]. While these adjustments are technical rather than structural, they are crucial for ensuring accuracy and assurance in reporting. This interconnected framework highlights the GHG Protocol’s central role in emissions accounting, forming the backbone of reliable ESG reporting.

"For organisations with a GHG Protocol-aligned inventory, CSRD does not replace the calculation work - it wraps it in a legally binding disclosure structure." - GreenCalculus [11]

What the GHG Protocol Means for Private Markets Due Diligence

In earlier discussions, the GHG Protocol's role as a regulatory benchmark was outlined. For private equity deal teams, its alignment is a key element in ensuring the reliability of emissions data.

But beyond just ticking regulatory boxes, the GHG Protocol provides crucial insights into private markets.

Using the GHG Protocol in ESG due diligence

When evaluating a target company's climate risks, aligning with the GHG Protocol serves as the foundational test for comparability. Its structured approach to Scopes 1, 2, and 3 emissions allows for meaningful comparisons between businesses. Without this framework, emissions data often stem from inconsistent and incompatible assumptions.

The protocol's five guiding principles - Relevance, Completeness, Consistency, Transparency, and Accuracy - act as a checklist to confirm that a company's emissions inventory accurately represents its operations. For example, it's vital to check if both location-based and market-based Scope 2 emissions are reported. Leaving out either could obscure the company's actual energy procurement practices [7].

Common problems in emissions reporting

Several recurring issues tend to arise during emissions reviews in private equity deals:

- Organisational boundaries: Often, companies define their boundaries inconsistently, excluding subsidiaries or joint ventures without clear reasoning.

- Scope 3 gaps: Incomplete Scope 3 reporting is a frequent issue. Since value chain emissions can account for up to 90% of a company's carbon footprint, failing to include or justify exclusions from Scope 3 categories undermines the data's credibility. The GHG Protocol outlines 15 Scope 3 categories, and a robust inventory should at least screen all of them, explaining any exclusions based on materiality.

-

Avoided emissions claims: Be cautious of claims about avoided emissions. These often cannot be verified. As the GHG Protocol notes:

Such claims are outside the standard emissions inventory framework and should not be treated as offsets for a company's actual emissions."Corporations are increasingly claiming that their goods and services reduce emissions. But there is a big problem: These avoided emissions claims are often unverifiable or inaccurate." - GHG Protocol [12]

To address these challenges, Axion Lab provides tools that simplify due diligence by applying rigorous GHG Protocol standards.

How Axion Lab applies GHG Protocol analysis

Axion Lab's AI platform is designed to streamline private market due diligence by focusing on GHG Protocol alignment. It examines sustainability reports, CDP responses, and management presentations to evaluate compliance across Scopes 1, 2, and 3. The platform identifies gaps in organisational boundaries, incomplete Scope 3 coverage, and methodological inconsistencies - issues that typically require extensive manual effort to uncover.

For financial and holding companies, the platform pays particular attention to Scope 3's Category 15 (Investments), which is crucial for understanding portfolio-level climate impacts in private equity [12]. By processing documents five to ten times faster than traditional methods, the AI delivers structured insights efficiently while maintaining adherence to GHG Protocol standards. Every deliverable is reviewed by a senior sustainability partner to ensure the findings are tailored to the specific context.

Conclusion: The GHG Protocol as the Basis for Every Footprint

The GHG Protocol serves as the cornerstone for nearly all major sustainability frameworks. While standards like CSRD, CDP, SBTi, ISSB, and ISO 14064 each bring their own nuances, they all rely on the same measurement principles. This shared foundation is highlighted by the fact that 97% of S&P 500 companies adhere to it, showcasing its widespread global acceptance [2]. For private markets, it provides deal teams with a reliable method to validate emissions data. Elements such as scope boundaries, category coverage, and calculation methods are all rooted in the protocol. Inventories that stray from or fail to document this approach are essentially unverifiable. As the protocol evolves, its role in due diligence becomes even more critical.

The Scope 3 Standard is undergoing a comprehensive revision, with the updated version expected by late 2027 [13]. Proposed updates, such as a mandatory 95% coverage threshold and requirements for data disaggregation, will set a higher standard for credible emissions inventories. Deal teams well-versed in the protocol will be better equipped to navigate these changes and assess compliance as these stricter requirements come into play. As confirmed by leading sources, the GHG Protocol remains the most widely adopted greenhouse gas accounting standard worldwide [1][2].

Understanding the GHG Protocol is crucial for interpreting emissions data, evaluating climate targets, and analysing sustainability disclosures. This framework provides the backbone for various reporting standards and supports thorough due diligence processes - whether reviewing a CDP submission, examining an ESRS E1 report, or evaluating a portfolio company's net-zero strategy.