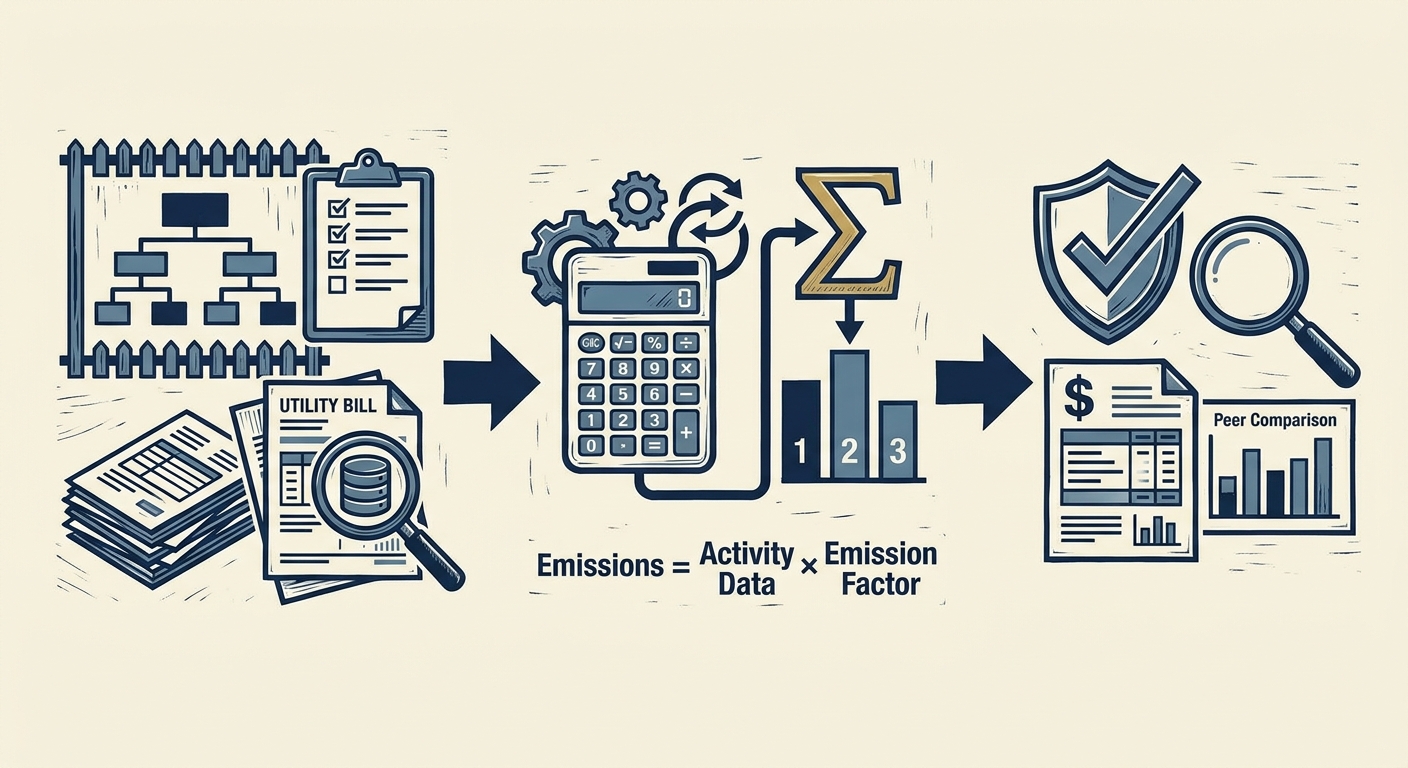

Calculating your company’s carbon footprint can feel complex, but it boils down to six clear steps. Here’s a quick breakdown:

- Set Boundaries: Define which parts of your business (organisational and operational) are included. Choose between equity share, financial control, or operational control approaches.

- List Activities: Identify all emissions-generating activities across Scopes 1, 2, and 3. Scope 3 often accounts for 70–90% of total emissions.

- Gather Data: Collect accurate data for each activity. Use primary data (e.g., utility bills, fuel logs) wherever possible and secondary data if necessary.

- Choose Emission Factors: Apply the correct emission factors (e.g., DEFRA’s UK conversion factors) to convert activity data into emissions (kg CO₂e).

- Calculate Totals: Sum emissions by scope (1, 2, and 3) and by category for Scope 3. Include dual reporting for Scope 2 (location- and market-based).

- Validate Results: Cross-check emissions against financial records, peer benchmarks, and operational metrics. Document all assumptions and exclusions.

This process ensures your carbon footprint is accurate, transparent, and ready for audits or regulatory compliance. The key is thorough documentation and using reliable data sources.

How to Calculate Your Company's Carbon Footprint: 6-Step Guide

Step 1: Set Your Organisational and Operational Boundaries

The first step in measuring your carbon footprint is deciding which assets and operations to include. The Greenhouse Gas (GHG) Protocol breaks this process into two key areas: organisational boundaries (which legal entities and assets you include) and operational boundaries (which emission sources within those entities you account for). These definitions form the foundation for every calculation that follows.

Organisational Boundaries

The GHG Protocol outlines three approaches to determine which entities - such as subsidiaries, joint ventures, or partnerships - should be included in your inventory [2].

| Consolidation Approach | Explanation |

|---|---|

| Equity Share | Report emissions based on your ownership stake. For example, owning 40% of a joint venture means you include 40% of its emissions. |

| Financial Control | Include 100% of emissions from entities where you control financial and operational decisions to gain economic benefits. |

| Operational Control | Include 100% of emissions from operations where you have the authority to implement policies and procedures. |

The operational control method is the most widely used.

"The operational control approach is the most common: it typically aligns best with what an organisation feels it is responsible for, and it also often leads to the most comprehensive inclusion of assets in the inventory." - US EPA [2]

If aligning GHG reporting with financial statements is your priority, the equity share or financial control approaches may be more suitable. For organisations with complex ownership structures, the equity share method often provides a more accurate reflection of economic interests. One key implication of this choice is its impact on Scope 3 accounting: for instance, emissions from a joint venture excluded under a control-based approach would instead be accounted for under Scope 3 (Category 15: Investments).

Operational Boundaries

Once you've determined which entities are within scope, the next step is identifying the emission sources within them. This is where Scopes 1, 2, and 3 come into play.

- Scope 1: Direct emissions from sources owned or controlled by your organisation, such as fuel combustion in company-owned boilers, vehicles, or refrigerant leaks.

- Scope 2: Indirect emissions from purchased energy, including electricity, district heating, or steam.

- Scope 3: Other indirect emissions across your value chain, such as those linked to the procurement of goods and services, business travel, waste disposal, and the use or disposal of products.

A simple way to think about it: if you control the asset or operation, it belongs in Scope 1 or 2. If you don’t, it falls under Scope 3. The treatment of leased assets also depends on the consolidation approach you choose. For example, under operational control, operating leases are included in Scope 1 or 2. Under equity share or financial control, they are assigned to Scope 3 [2][3].

Establishing these boundaries ensures clarity and consistency for the decisions you’ll make later.

Where Judgement Plays a Role

Defining boundaries requires careful judgement, and these decisions must be documented thoroughly. The consolidation approach you select reflects your organisation’s accountability and can shape how your results are perceived by stakeholders and auditors.

For Scope 3, all 15 categories must be screened to determine which are material enough to include. Assessing materiality involves considering the scale of emissions, your ability to influence them, and their relevance to stakeholders.

To formalise your decisions, draft a boundary memo that lists each entity, the chosen consolidation method, ownership percentage, and the rationale for inclusions or exclusions. This memo should be approved by senior leadership, such as your CFO or COO, to ensure alignment across the organisation.

sbb-itb-6ca8558

Step 2: List Your Emissions-Relevant Activities

Once you've set your boundaries, the next step is identifying all the emissions-generating activities within those boundaries. Think of this as gathering the raw materials for your calculations. The more thorough you are here, the stronger your final carbon footprint assessment will be.

Activity Mapping Across Scopes

Each activity links back to the boundaries defined in Step 1. Activities under your direct control fall into Scope 1 or 2, while those within your value chain but outside direct control are assigned to Scope 3.

| Scope | Typical Activity Examples |

|---|---|

| Scope 1 | Natural gas boilers, company-owned vehicle fleets, refrigerant refills, process emissions (e.g., gas bills, fuel card data, maintenance logs) |

| Scope 2 | Purchased electricity, district heating, steam (e.g., electricity bills in kWh, energy contracts) |

| Scope 3 Upstream | Purchased goods and services, business travel, employee commuting, waste disposal (e.g., ERP spend data, expense claims, waste transfer notes) |

| Scope 3 Downstream | Third-party logistics, use of sold products, end-of-life treatment, investments (e.g., shipping manifests, product specs, sales data) |

Scope 3 often requires extra attention. On average, value chain emissions make up 75% of a company's total carbon footprint [3], with some estimates reaching as high as 90% [4]. The GHG Protocol breaks Scope 3 into 15 categories, covering upstream and downstream activities [3][4]. Skipping this scope means leaving the bulk of your climate impact unaddressed.

Once you've mapped out your activities, it's time to evaluate their importance.

Materiality Screening

The next step is prioritising activities by their significance. A practical way to start is by screening all 15 Scope 3 categories using spend-based data - this involves multiplying financial expenditure by an average emissions factor. This approach helps you identify major emission sources without needing detailed data upfront.

"The GHG Protocol recommends screening all 15 categories to identify which are material, then prioritizing data collection and calculation for the most significant ones." - Konstantinos Kouzelis, Founder & CEO, Coolset [4]

After estimating the size of each category, assess materiality using four criteria: magnitude (the volume of emissions), influence (your ability to reduce emissions), regulatory risk (potential exposure to carbon taxes or stricter regulations), and stakeholder interest (areas under scrutiny from investors or customers). For many companies, the largest contributors are usually Category 1 (Purchased Goods & Services) and Category 11 (Use of Sold Products) [3].

If you decide to exclude activities below the materiality threshold, document your reasons in writing. The GHG Protocol's completeness principle requires all exclusions to be explicitly disclosed [4].

Building an Activity Register

Organise your findings into a traceable activity register - a structured document that ensures your inventory is ready for audit. Each entry should include the business unit, activity description, scope, GHG Protocol category, data source, and materiality ranking.

To avoid errors, create a data dictionary alongside your register. This dictionary should define standard units for each activity type - like energy in kWh or mass in kg - and list approved conversion factors. Mistakes in units are a common cause of inventory issues [3], and a data dictionary helps prevent them. Assign a simple data quality score (1–5) to each entry: 1 for verified primary data and 5 for incomplete or untraceable sources. This scoring system highlights where to focus your data collection efforts in the next step.

Step 3: Gather Activity Data

Now that your activity register is set up, the next step is to populate it with accurate data. At this stage, carbon accounting becomes just as much about managing data as it is about environmental impact.

Primary and Secondary Data Sources

The accuracy of your carbon footprint hinges on the quality of the data you input. Whenever possible, aim to use primary data - information directly sourced from your operations or verified by suppliers.

For Scope 1, this means using records like gas meter readings, fuel card logs, and refrigerant maintenance reports that track the kilograms of gas added. For Scope 2, primary data includes electricity bills with kWh readings and meter IDs, as well as Guarantees of Origin (GOs) if you're following a market-based reporting method. Scope 3 data tends to be more varied, drawing from systems like ERP and procurement platforms, freight forwarder reports (tracking ton-kilometres by route and mode), travel management systems, waste contractor receipts, and even metrics from cloud or IT services.

If primary data isn’t available, secondary data - such as sector averages or spend-based estimates - can fill in the gaps. The table below provides a quick reference for common activities and their ideal data sources:

| Scope | Activity | Recommended Data Source | Units to Collect |

|---|---|---|---|

| Scope 1 | Stationary combustion | Gas bills, meter readings | m³ or kWh |

| Scope 1 | Mobile combustion | Fuel cards, odometer logs | Litres, km |

| Scope 1 | Fugitive emissions | Maintenance/service reports | kg (refrigerant topped up) |

| Scope 2 | Purchased electricity | Utility bills, energy contracts | kWh, MWh |

| Scope 3 | Purchased goods | ERP/procurement spend data | £, kg of material |

| Scope 3 | Logistics | Freight forwarder reports | Ton-km, route, mode |

| Scope 3 | Business travel | Travel agency logs, expense claims | Flight routes, hotel nights |

| Scope 3 | Waste | Waste contractor receipts | kg by fraction/treatment |

Once you’ve identified the data sources, the next step is to standardise the units across your register for consistency.

Standardising and Checking Data

Raw data often comes in a mix of units - gas bills might use standard cubic metres (Smc), fuel invoices list litres, and steam records might show tonnes. Before you apply any emission factors, you’ll need to convert everything into consistent metric units, such as energy in kWh or MWh and mass in kilograms or tonnes.

"The most expensive errors are almost always unit errors." - CarbonMeld

To avoid these pitfalls, create a data dictionary. This document serves as a central reference, listing the standard units and approved conversion factors for your organisation. Once your data is standardised, cross-check it against financial records. For example, compare fuel litres to invoices or meter readings to utility bills. For vehicle fleets, calculate fuel efficiency in litres per 100 km, and for buildings, check energy use in kWh per square metre. Any outliers you spot during this process could indicate missing data or double entries.

Judgement in Data Selection

In some cases, collecting primary data - especially for Scope 3 - isn’t practical. When this happens, use spend-based estimates (financial spend multiplied by an economic input-output emission factor) for smaller, lower-impact suppliers. Reserve the more detailed physical activity data for your largest-impact categories.

It’s essential to document your approach. Clearly note which activities use primary data, which rely on sector averages, and which use proxies. Include the rationale for these choices so your assumptions are transparent to auditors and your team for future reporting cycles.

"If you don't measure quality, you won't improve it." - CarbonMeld

With your data standardised and checked for quality, you’ll be ready to move on to applying emission factors in the next step.

Step 4: Choose Your Emission Factors

Once you have standardised your activity data, the next step is to convert these figures into emissions. This is done using a coefficient called the emission factor.

What Emission Factors Are

An emission factor is a value that represents the greenhouse gases produced per unit of activity, typically measured in kg CO₂e per unit. For instance, burning natural gas emits 0.18290 kg CO₂e per kWh consumed (based on DEFRA's 2025 figures, Gross Calorific Value (GCV) basis) [8]. To calculate emissions, you simply multiply your activity data by the relevant emission factor. These factors are updated annually by recognised organisations. In the UK, or for those following Streamlined Energy and Carbon Reporting (SECR), the UK Government GHG Conversion Factors (published by DEFRA/DESNZ) are the standard reference [5].

These conversion factors are available in three formats:

- Condensed set: Ideal for most users.

- Full set: Useful for advanced users managing large datasets.

- Flat file: Designed for automated processing [6].

For most in-house reporting teams, starting with the condensed set is the simplest and most practical approach.

"The conversion factor spreadsheets provide the values to be used for such conversions, and step by step guidance on how to use them." - GOV.UK [5]

One key rule: always use the emission factors from your reporting year. Using factors from the wrong year can lead to significant errors. For example, the UK grid emission factor dropped from 0.20705 kg CO₂e/kWh in the 2024 dataset to 0.177 kg CO₂e/kWh in the 2025 dataset - a 15% reduction in just one year [7]. Using outdated figures would skew your results, especially for electricity emissions.

Applying the Activity × Factor Formula

The formula for calculating emissions is simple:

Emissions (kg CO₂e) = Activity Data × Emission Factor

Let’s say your organisation consumed 2,500,000 kWh of electricity during the reporting year. Using the DEFRA 2025 location-based factor of 0.177 kg CO₂e/kWh, your calculation would be:

2,500,000 kWh × 0.177 kg CO₂e/kWh = 442,500 kg CO₂e (or 442.50 tCO₂e) [7].

This result reflects your Scope 2 location-based electricity emissions. The same approach applies to all activities in your emissions register, whether it’s diesel consumption, waste disposal, or business travel. For each, you multiply the activity data by the relevant factor.

It’s essential to ensure that the calorific value basis of your activity data matches the emission factor. For example, discrepancies in the GCV basis for natural gas can introduce up to a 10% error [8]. Accuracy here sets the stage for the final summation and validation in later steps.

Judgement in Factor Selection

Choosing the right emission factors involves careful decision-making.

For Scope 2 electricity, the main decision is whether to use a location-based or market-based factor. The location-based factor reflects the average emissions intensity of the physical grid, which for the UK in 2025 is 0.177 kg CO₂e/kWh [7]. On the other hand, market-based factors account for contractual procurement, often showing lower emissions when verified zero-emissions tariffs are used. However, the GHG Protocol requires both figures to be reported. The location-based total provides a baseline against which any contractual claims are measured [7].

"The location-based total is never suppressible - it is the answer to 'what would your Scope 2 footprint be without any contractual claims' and serves as the anchor against which market-based progress is measured." - Jeremiah Say, Lead Systems Architect, GreenCalculus [7]

For Scope 3 emissions, the judgement lies between using generic national factors or supplier-specific data. Where possible, prioritise verified data from suppliers, especially for high-impact categories like logistics or manufacturing. For smaller suppliers, where primary data isn’t available, national or sector averages are an acceptable fallback. Always document the reasoning behind your choices and focus on obtaining the most precise factors for activities with the greatest impact.

Step 5: Calculate and Sum Emissions by Scope

Using the emission factors selected in Step 4, it's time to calculate emissions for each activity to create a full picture of your company's carbon footprint.

Line-by-Line Calculations

For each activity, the formula is straightforward: Emissions (kg CO₂e) = Activity Data × Emission Factor. Keep a detailed log that includes the activity data, the emission factor used, and the resulting emissions. This level of documentation allows you to cross-check figures against original records, such as fuel cards, utility bills, or refrigerant logs.

If your activities involve gases like methane or nitrous oxide, you'll need to convert them into CO₂e using the IPCC AR6 GWP values. For example, AR6 assigns a GWP of 29.8 to fossil methane, slightly different from the AR5 value of 30 [8].

"Manually-typed numbers in ESG reports are the single biggest source of restatement risk." - SmartQHSE [9]

To minimise errors and the risk of needing to revise reports, consider automating data collection. Use an audited pipeline that pulls directly from source systems, ensuring accuracy and reducing manual input.

Aggregating by Scope and Category

Once you've calculated emissions for individual activities, organise them by Scope 1, Scope 2, and Scope 3. Here's how to approach each scope:

- Scope 1: Sum all direct emissions, including stationary combustion, mobile combustion, process emissions, and fugitive releases.

- Scope 2: Provide two totals - one based on location and another based on market data - as required by the GHG Protocol [9].

- Scope 3: Group emissions by category, following the GHG Protocol's 15-category framework. Separate upstream and downstream activities, and if a category is excluded due to materiality, document the reasoning clearly. Remember, Scope 3 often accounts for 70–90% of a company's total emissions [1].

| Scope | Key Sources | Reporting Requirement |

|---|---|---|

| Scope 1 | Fuel cards, refrigerant logs, combustion meters | Direct emissions by source category |

| Scope 2 | Utility invoices, PPAs | Dual reporting: location-based and market-based |

| Scope 3 | Procurement ledgers, travel logs, contractor data | Reported by category (1–15) |

Adding Intensity Metrics

While absolute totals provide a clear picture of your overall emissions, intensity metrics (e.g., tCO₂e per £m revenue or per full-time employee) help measure operational efficiency [9]. These metrics are particularly relevant for UK businesses reporting under SECR or submitting Carbon Reduction Plans under PPN 06/21, as they link environmental performance to business outcomes.

Make sure the 12-month period for your emissions data aligns with the period used for your denominator (such as annual revenue or average employee headcount). Clearly document both your emissions calculation methodology and the source of your denominator data to ensure your metrics can withstand audits or supplier reviews [1].

With your emissions totals and intensity metrics in hand, you're ready to move on to validating your data in the next step.

Step 6: Sanity-Check Your Results

Once you've calculated your emissions totals, the next step is to make sure they hold up under scrutiny. A carbon footprint that looks good on paper but doesn’t align with how your business actually operates could raise red flags - whether from auditors, procurement teams, or environmentally aware investors.

Checking Results Against the Business Model

Start by comparing your activity data to your financial records. Then, calculate simple operational metrics like kWh per square metre for office spaces or litres per 100 km for your fleet. These ratios should match your real-world operations [3].

It’s also helpful to review year-on-year changes while factoring in variables like production volume, working days, or occupancy levels. For example, if your emissions increase unexpectedly but your headcount or revenue remains steady, you'll need to dig deeper before finalising your report [3].

"An 'audit-ready' inventory is one that can be reconstructed. If in 6 months someone asks 'where does this number come from?', you must be able to answer with files, sources, and rules." - CarbonMeld [3]

Benchmarking Against Sector Peers

Once your figures are internally consistent, compare your intensity metrics to industry averages. This benchmarking step helps confirm your data’s reliability. For instance, if your electricity emissions don’t align with typical grid benchmarks, double-check that you’ve used the correct DEFRA factor for the year - DEFRA updates these factors every June [11].

Recording Adjustments and Assumptions

Document any changes or assumptions made during your review. This includes the consolidation boundary you used - whether equity share, financial control, or operational control - and the reasoning behind excluding any Scope 3 categories. Record the vintage of each emission factor and note any proxies used when primary data wasn’t available [10]. Establishing a formal recalculation policy is also crucial. For example, you might decide to recalculate your base year if a methodology change shifts emissions by more than 5% [10].

Here’s a quick look at common reasons carbon footprints fail audits and how this step can help catch them:

| Common Audit Rejection | Why It's Flagged |

|---|---|

| Single-figure Scope 2 | Omitting both location-based and market-based figures [10] |

| Vintage mismatch | Using emission factors from a different year than the activity data [10] |

| Undocumented base year | Setting targets without declaring a base year or recalculation policy [10] |

| Missing materiality rationale | Excluding Scope 3 categories without a documented screening process [10] |

"Scope 3 errors are the most common cause of Carbon Reduction Plans being questioned or rejected - particularly under PPN 06/21 procurement reviews." - Frazer Holroyd, Carbon Consultant and Founder, The Carbon Stamp [1]

Conclusion: What Makes a Footprint Defensible

A carbon footprint is defensible not just when the calculations are done, but when every choice behind those calculations can be clearly explained and backed up. The process involves defining boundaries, mapping activities, collecting high-quality data, selecting appropriate emission factors, and validating the results. Every decision at each step must be documented and justified.

Strong carbon footprint calculations rely on careful judgement at every stage. For example, when setting organisational boundaries, did you use financial, operational, or equity control? Have you made exclusions in Scope 3 clear, and have you applied factors like the DEFRA-recommended 1.9 multiplier for aviation emissions? These choices ultimately determine whether your inventory can withstand scrutiny during procurement reviews, external audits, or under regulatory frameworks like the CSRD.

"The hard part isn't 'doing the math.' It's deciding boundaries, data, and rules in a consistent way - so the result stands up to an audit and is actually useful for reducing emissions." - CarbonMeld [3]

The quality of your data is equally vital. Using primary data, such as direct measurements, utility invoices, or supplier declarations, adds significant credibility compared to relying on spend-based proxies [12][1]. Since Scope 3 often represents the majority of a company’s carbon footprint [1], basing calculations on rough economic proxies for key categories can weaken an otherwise strong inventory.

"Where that lineage is weak, the assurer flags it; where it is strong, the consolidated report becomes defensible." - SmartQHSE [9]