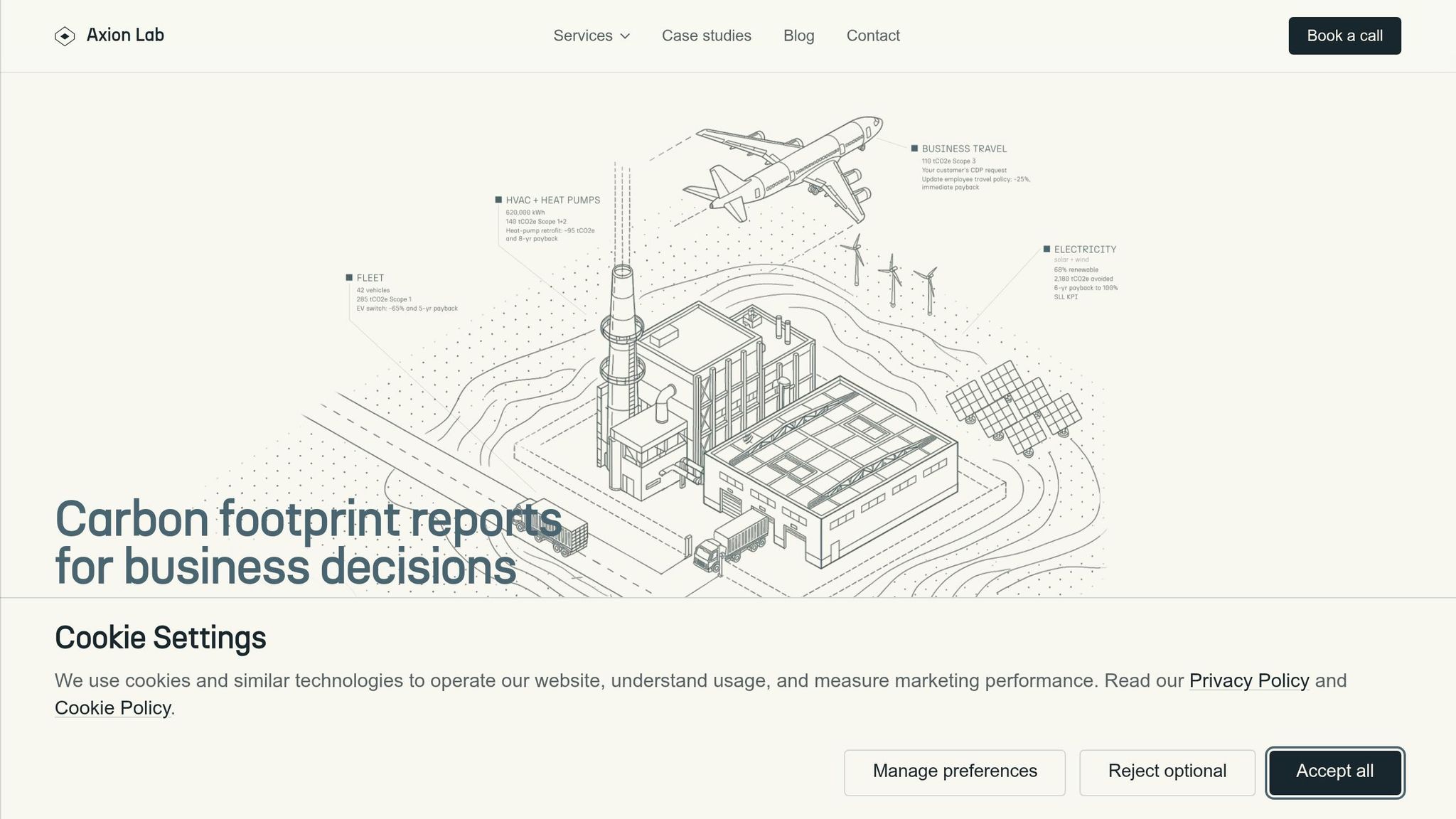

Scope 3 emissions are the largest part of most companies' carbon footprint, often making up 65–95% of total emissions. These emissions are divided into 15 categories under the GHG Protocol, covering everything from supplier emissions to product use and disposal. However, not all categories are equally important. Typically, just 2–4 categories dominate a company's emissions, with Purchased Goods & Services (Category 1) and Use of Sold Products (Category 11) accounting for around 84% globally.

To effectively manage Scope 3 emissions, businesses should:

- Start with a materiality screening to identify which categories matter most.

- Focus on the high-impact areas specific to their sector.

- Use tools like AI-driven platforms to streamline data collection and analysis.

For example:

- Manufacturers focus on supplier emissions (Category 1) and product use (Category 11).

- Financial institutions prioritise financed emissions (Category 15).

- Professional services often see most emissions from business travel (Category 6) and commuting (Category 7).

All 15 Scope 3 Categories At A Glance

The GHG Protocol breaks Scope 3 emissions into eight upstream categories (1–8) and seven downstream categories (9–15). Upstream categories involve activities before a product reaches the customer, while downstream categories focus on what happens after the customer receives it. Below, you'll find a handy reference list of all 15 categories, providing a quick overview before diving deeper into their importance in later sections.

As Paul Ferreira puts it:

"One company's downstream Scope 3 emissions are another company's upstream Scope 3 emissions." [1]

This interconnectedness is precisely why the framework is so essential.

Here’s a table summarising each category’s definition, its position in the value chain, and its typical relevance:

| # | Category | Direction | One-Line Definition | Typical Materiality |

|---|---|---|---|---|

| 1 | Purchased Goods & Services | Upstream | Emissions from producing and transporting everything your company buys | High |

| 2 | Capital Goods | Upstream | Emissions from manufacturing machinery, buildings, and IT equipment you purchase | Medium/High |

| 3 | Fuel- & Energy-Related Activities | Upstream | Extraction and transmission losses for purchased fuels and electricity not in Scope 1 or 2 | Medium |

| 4 | Upstream Transport & Distribution | Upstream | Third-party logistics moving goods to your operations | High |

| 5 | Waste Generated in Operations | Upstream | Disposal and treatment of waste produced in your facilities | Low/Medium |

| 6 | Business Travel | Upstream | Employee travel via air, rail, or road using third-party vehicles, including hotels | Medium/High |

| 7 | Employee Commuting | Upstream | Emissions from staff travelling between home and the workplace | Low/Medium |

| 8 | Upstream Leased Assets | Upstream | Operation of assets leased from others, not included in Scope 1 or 2 | Low |

| 9 | Downstream Transport & Distribution | Downstream | Third-party logistics moving finished products to customers | Medium/High |

| 10 | Processing of Sold Products | Downstream | Further processing of your intermediate products by third-party customers | Low/Medium |

| 11 | Use of Sold Products | Downstream | Energy or GHG emissions generated when customers use your product over its lifetime | High |

| 12 | End-of-Life Treatment | Downstream | Disposal, recycling, or incineration of products after customer use | Medium |

| 13 | Downstream Leased Assets | Downstream | Operation of assets you own but lease out to others | Medium (sector-specific) |

| 14 | Franchises | Downstream | Scope 1 and 2 emissions from your franchisees | High (franchisors only) |

| 15 | Investments | Downstream | Financed emissions from equity, debt, and project finance | High (financial sector) |

This breakdown helps identify where to focus when assessing emissions, especially during due diligence or materiality screening.

Interestingly, Category 1 (Purchased Goods & Services) and Category 11 (Use of Sold Products) dominate the Scope 3 landscape, together accounting for about 84% of all reported emissions globally [4][6]. This is why they consistently top materiality assessments. On the other hand, categories like Upstream Leased Assets (Category 8) and Processing of Sold Products (Category 10) are often less relevant for most businesses.

It’s important to note that these materiality levels are general guidelines, not universal rules. For instance, while a software company might see negligible emissions in Category 11, an automotive manufacturer could find it to be their largest contributor. Later sections will dive into sector-specific examples and explain why understanding materiality is a critical first step before measurement.

Which Categories Usually Dominate

When it comes to Scope 3 emissions, only a handful of categories tend to have a major impact. In fact, Category 1 (Purchased Goods & Services) and Category 11 (Use of Sold Products) combined account for roughly 84% of globally reported Scope 3 emissions. This concentration means most companies focus their measurement and reduction efforts on these two categories [6].

Category 1 is often the largest contributor for many businesses. This is particularly true for industries like food, agriculture, and electronics manufacturing, where complex supply chains embed significant carbon emissions from raw materials and processing. A striking example comes from Apple: in April 2025, the company revealed that its Supplier Clean Energy Programme, involving over 300 suppliers, had helped achieve a 55% reduction in manufacturing-related Scope 3 emissions since 2015 [2]. This upstream focus highlights the contrast between the emissions from production (Category 1) and those from product use (Category 11).

Category 11, on the other hand, focuses on emissions generated during the use of a product over its lifetime, rather than those tied to its production. For sectors like automotive and electronics, this category often dominates because vehicles and appliances typically produce far more emissions during use than during manufacturing. Meanwhile, Category 4 (Upstream Transport & Distribution) is particularly relevant for industries reliant on logistics. For instance, switching freight modes can cut emissions by as much as 50% [1].

Category 2 (Capital Goods) also deserves attention, especially in asset-heavy industries like construction and heavy manufacturing. Its significance lies in the fact that the full emissions of a capital asset are recorded in the year it is acquired, rather than being distributed across its lifespan [1].

For financial institutions, the picture is quite different. Here, Category 15 (Investments) takes centre stage, often overshadowing all other Scope 3 categories. This category covers emissions from financed activities, such as loans and equity portfolios. For instance, JPMorgan Chase uses the PCAF standard to track financed emissions across sectors like oil, gas, power, and auto manufacturing, setting specific decarbonisation goals for each [2].

"The scale of Category 15 can make all other scope 3 categories appear marginal. For financial institutions, it is typically the defining category." - Normative [1]

Categories That Are Often Low Priority

Using a thorough materiality screen helps pinpoint which areas deserve detailed measurement and which can be deprioritised. This approach works hand-in-hand with ranking dominant categories, ensuring that sector-specific materiality shapes the focus of measurement efforts.

Not all Scope 3 categories demand the same level of attention. Categories like 1 (Purchased Goods and Services) and 11 (Use of Sold Products) often dominate a business's carbon footprint. On the other hand, some categories, after materiality screening, are found to have minimal impact. For instance, waste generated in operations (Category 5) generally contributes only 1–3% of a company’s total emissions [4].

Similarly, Category 8 (Upstream Leased Assets) is often already included in Scope 1 and 2 reporting, making it redundant for many organisations [4]. Category 10 (Processing of Sold Products) is typically relevant only to intermediate goods producers, so it's rarely significant for software companies or direct-to-consumer brands.

"A software company will have negligible Category 10 emissions... while a car manufacturer's Category 11 will dominate its entire carbon footprint." - Paul Ferreira, Associate Climate Strategy Advisor, Normative [1]

Category 14 (Franchises) is another example of a low-priority area, as it’s irrelevant for most organisations that don’t operate under a franchise model [1].

It’s also important to avoid falling into the "easy data" trap. Categories like business travel (Category 6) and employee commuting (Category 7) often have readily available data, but their actual contribution to emissions can be overstated. For example, in industries such as manufacturing or construction, emissions are dominated by raw materials and logistics, making these categories almost negligible. However, for professional services firms, these two categories can account for 60–80% of Scope 3 emissions [4].

Ultimately, the focus on low-impact categories reinforces the importance of tailoring measurement efforts to areas that significantly drive emissions. This is why a materiality screen is a critical first step, ensuring that assessment efforts align with the realities of each sector.

Why Materiality Screening Comes Before Measurement

Focusing on the most impactful categories is crucial, and that's where materiality screening steps in before diving into measurement.

Attempting to measure all 15 Scope 3 categories is not only inefficient but also counterproductive. It drains resources and creates an inventory that might look thorough but fails to target the most significant emissions sources. The GHG Protocol's Corporate Value Chain (Scope 3) Standard directly addresses this by requiring companies to evaluate all 15 categories first. For any exclusions, they must provide documented justification [8]. This ensures transparency and avoids selective reporting, where only easily accessible data is included while emissions-heavy categories are ignored.

A well-executed materiality screen narrows the focus to the 3–5 categories that usually account for 80–90% of total emissions [5]. This allows for concentrated efforts on intensive data collection, such as obtaining primary supplier data or using activity-based measurements. For categories deemed less critical, simpler methods like spend-based estimates are sufficient.

"Scope 3 emissions typically represent 70–90% of a business's total carbon footprint. Ignore them, and you're ignoring most of your climate impact." - Frazer Holroyd, Carbon Consultant and Founder, The Carbon Stamp [3]

The GHG Protocol defines materiality beyond just the size of emissions. A category is considered material if a company has significant influence over it, if it offers credible opportunities for reduction, or if stakeholders have expressed concerns about it. Reporting frameworks like CDP - which saw over 23,000 companies disclose in 2024 - consider any category exceeding 5% of the estimated total Scope 3 footprint as material [5]. Regulatory requirements are also pushing companies to take this seriously. The EU's CSRD (under ESRS E1) and California's SB 253 mandate disclosure of material Scope 3 categories, making this process a legal obligation for many large firms, not just a best practice [5][7]. Beyond compliance, this approach enhances due diligence by sharpening the focus on what truly matters.

Materiality screening is equally critical in due diligence processes. For private market investors, it highlights which value chain activities pose the highest transition risks or offer the greatest potential for decarbonisation before finalising deals. Tools like Axion Lab streamline this process by automating the initial due diligence. By applying spend-based and industry-average emission factors to financial data, these tools quickly pinpoint which categories need deeper investigation across diverse portfolios. This AI-driven approach is especially useful when assessing multiple assets simultaneously, where manual analysis would be far too slow.

sbb-itb-6ca8558

How Categories Rank Across Sectors

All 15 Scope 3 Categories Ranked by Materiality Across Sectors

When looking at Scope 3 emissions across different sectors, just two categories account for a whopping 81% of total emissions [4]. The table below highlights priority tiers by sector, giving a clear snapshot of which categories matter most.

A major factor in emissions distribution is whether a company operates upstream or downstream in the value chain. For instance, manufacturers and retailers typically see the bulk of their emissions in Category 1 (Purchased Goods and Services), as the carbon footprint is tied to what they procure. On the other hand, fossil fuel companies face significant downstream emissions in Category 11 (Use of Sold Products) - combustion alone makes up 80–90% of their Scope 3 emissions [4]. Financial institutions, meanwhile, often have nearly all (99.98%) of their emissions in Category 15 (Investments) [4].

The type of product a company deals with also plays a big role. Energy-intensive products like electronics, vehicles, or industrial equipment are heavily tied to Category 11, while less energy-intensive items like clothing or professional services mostly fall under Category 1 [4]. For professional services, Categories 6 (Business Travel) and 7 (Employee Commuting) can account for 60–80% of Scope 3 emissions [4], making purchased goods less of a priority.

Here’s a breakdown of priority tiers for six key sectors, based on GHG Protocol sector guidance and CDP data patterns:

| Sector | High Priority | Medium Priority | Low/Immaterial |

|---|---|---|---|

| Manufacturing | Cat 1 (Purchased Goods), Cat 11 (Use of Sold Products), Cat 4 (Upstream Transport) | Cat 2 (Capital Goods), Cat 5 (Waste), Cat 9 (Downstream Transport) | Cat 6 (Business Travel), Cat 7 (Commuting), Cat 14 (Franchises) |

| Technology | Cat 1 (Purchased Goods/Cloud), Cat 11 (Use of Sold Products) | Cat 6 (Business Travel), Cat 7 (Commuting), Cat 2 (IT Capital Goods) | Cat 10 (Processing), Cat 14 (Franchises), Cat 15 (Investments) |

| Financial Services | Cat 15 (Investments) | Cat 1 (Purchased Services), Cat 6 (Business Travel) | Cat 4 (Upstream Transport), Cat 5 (Waste), Cat 12 (End-of-Life) |

| Retail | Cat 1 (Purchased Goods), Cat 4 (Upstream Transport) | Cat 9 (Downstream Transport), Cat 12 (End-of-Life) | Cat 10 (Processing), Cat 13 (Downstream Leased Assets) |

| Construction | Cat 1 (Purchased Goods), Cat 2 (Capital Goods) | Cat 4 (Upstream Transport), Cat 5 (Waste) | Cat 11 (Use of Sold Products), Cat 14 (Franchises) |

| Professional Services | Cat 6 (Business Travel), Cat 7 (Employee Commuting) | Cat 1 (Purchased Services/Cloud) | Cat 2 (Capital Goods), Cat 11 (Use of Sold Products) |

For example, a construction company with a large fleet might find Category 4 (Upstream Transport) nearly as critical as Category 1 (Purchased Goods). Similarly, a tech firm with substantial venture investments may need to focus more on Category 15 (Investments). These tiers provide a useful starting point for tailoring priorities to specific industries.

Summary Table: All 15 Categories

The breakdown above highlights how priorities vary based on what a company produces and sells. Below is a summary table that captures each category's position, typical materiality, and high-priority sectors. It serves as a quick reference for understanding sector-specific materiality and where each category fits within the value chain.

Note: Materiality bands are general guidelines. A "low" rating might still be relevant for unique business models. Categories 13 and 14 apply only to specific types of businesses, while Category 15 deserves special focus. As Normative points out, "the scale of Category 15 can make all other Scope 3 categories appear marginal" [1] for financial institutions. This table condenses earlier discussions on materiality screening and sector priorities.

| # | Category | Direction | Typical Materiality | High-Priority Sectors (Typical) |

|---|---|---|---|---|

| 1 | Purchased Goods & Services | Upstream | Very High | Almost all sectors; Retail, Food & Agriculture, Electronics, Manufacturing |

| 2 | Capital Goods | Upstream | Medium/High | Manufacturing, Construction, Infrastructure, Mining |

| 3 | Fuel- & Energy-Related Activities | Upstream | Low/Medium | Energy-intensive industries, Logistics, Utilities |

| 4 | Upstream Transport & Distribution | Upstream | Medium/High | Retail, Manufacturing, Apparel, Distribution |

| 5 | Waste Generated in Operations | Upstream | Low/Medium | Manufacturing, Construction, Healthcare |

| 6 | Business Travel | Upstream | Medium (High for services) | Professional Services, Consulting, Large Corporates |

| 7 | Employee Commuting | Upstream | Low/Medium | Office-heavy businesses, Professional Services |

| 8 | Upstream Leased Assets | Upstream | Low | Logistics, Asset-heavy businesses |

| 9 | Downstream Transport & Distribution | Downstream | Medium/High | Manufacturers selling direct to consumers |

| 10 | Processing of Sold Products | Downstream | Medium | Chemicals, Steel, Intermediate goods producers |

| 11 | Use of Sold Products | Downstream | Very High | Automotive, Electronics, Appliances, Fossil Fuels |

| 12 | End-of-Life Treatment | Downstream | Low/Medium | Consumer Goods, Electronics, Apparel, Packaging |

| 13 | Downstream Leased Assets | Downstream | High (where applicable) | Real Estate, REITs, Property Managers |

| 14 | Franchises | Downstream | High (where applicable) | Fast Food, Hospitality, Retail Franchises |

| 15 | Investments | Downstream | Very High (Finance) | Banks, Asset Managers, Private Equity, Insurers |

A clear trend emerges: Categories 1 and 11 are dominant for most companies. This aligns with CDP data showing that these two categories alone account for 84% of all reported Scope 3 emissions globally [4]. Other categories often take a back seat unless flagged as material during screening.

How AI Tools Like Axion Lab Handle Scope 3 in Due Diligence

Manually reviewing all 15 Scope 3 categories can be a daunting task, especially when working under tight deal deadlines. AI-powered platforms like Axion Lab simplify this process, allowing deal teams to work more efficiently without sacrificing the depth of their analysis.

One key feature is automated document extraction. Instead of relying on analysts to manually comb through procurement records, AI tools handle the heavy lifting. They automatically extract monetary values and activity data, categorising each line item in line with the GHG Protocol. This data is then seamlessly integrated into a targeted spend-based screening process.

Building on initial materiality assessments, Axion Lab performs a spend-based screening across all 15 categories, homing in on the ones with the biggest impact. The system quickly identifies the top 3–5 emission categories that require further scrutiny, while documenting reasons for setting aside less relevant categories. This prioritisation is particularly valuable, as Categories 1 and 11 alone account for 84% of all reported Scope 3 emissions globally [4]. By focusing on these high-impact areas, deal teams can save a significant amount of time.

Another standout feature is data gap flagging. The platform highlights missing data and unclear reporting boundaries, such as supplier responses that fail to specify a timeframe or lack a methodology description [9]. These flagged issues help streamline the due diligence process by bringing attention to critical gaps early, giving teams the opportunity to request the necessary information before finalising deals.

For private equity firms adhering to SFDR and CSRD frameworks, this methodical approach also ensures compliance with audit requirements. Clearly documenting why certain categories are deemed immaterial - along with a transparent methodology - is just as important as the emissions data itself [4][5].

Conclusion

Focus on the most impactful Scope 3 categories. Across industries, just a few categories - often two or three - are responsible for the majority of emissions. The data highlights this clearly:

"The two most material Scope 3 categories in each sector cover, on average, 81% of total Scope 3 emissions. Accuracy in the key categories matters more than exhaustive perfection." [4]

Using a spend-based estimate to identify emissions hotspots ensures your efforts are both practical and focused. This targeted approach helps pinpoint where the bulk of emissions lie, allowing resources to be allocated efficiently while avoiding unnecessary data collection. Once these hotspots are identified, prioritise them and clearly document why other areas are set aside.

The key categories depend heavily on the sector. For example, electronics manufacturers might focus on the use of sold products, while financial institutions prioritise investments. There’s no universal ranking - only one that fits your specific business model.

These insights are especially valuable for teams working under tight deadlines. For private equity deal teams, the challenge intensifies with time constraints. This is where AI-powered tools like Axion Lab come into play. They simplify the initial screening process, highlight data gaps, and create audit-ready documentation compliant with CSRD and SFDR standards. This method ensures faster, defensible assessments without compromising on quality.

The importance of Scope 3 is only increasing, both from a regulatory and commercial perspective. Currently, just 38% of companies reporting to CDP have set Scope 3 reduction targets [10], leaving a significant gap between leaders and those falling behind. By homing in on the categories that have the biggest impact, businesses can streamline their due diligence processes while making meaningful progress towards decarbonisation goals.